If your company is a reporting company, your next step is to identify its beneficial owners. A beneficial owner is any individual who, directly or indirectly:

- Exercises substantial control over a reporting company;

- OR

- Owns or controls at least 25 percent of the ownership interests of a reporting company

An individual might be a beneficial owner through substantial control, ownership interests, or both. Reporting companies are not required to report the reason (i.e., substantial control or ownership interests) that an individual is a beneficial owner.

A reporting company can have multiple beneficial owners. For example, a reporting company could have one beneficial owner who exercises substantial control over the reporting company, and a few other beneficial owners who own or control at least 25 percent of the ownership interests of the reporting company. A reporting company could have one beneficial owner who both exercises substantial control and owns or controls at least 25 percent of the ownership interests of the reporting company. There is no maximum number of beneficial owners who must be reported

FinCEN expects that every reporting company will be substantially controlled by one or more individuals, and therefore that every reporting company will be able to identify and report at least one beneficial owner to FinCEN. The following four sections will assist you in determining your company’s beneficial owners. If an individual qualifies as a beneficial owner, information about that individual must be reported to FinCEN in a reporting company’s BOI report.

2.1 What is substantial control?

2.2 What is an ownership interest?

2.3 What steps can I take to identify my company’s beneficial owners?

2.4 Who qualifies for an exception from the beneficial owner definition?

This chapter generally covers 1010.380(d),“Beneficial owner”

Reporting companies are required to identify all individuals who exercise substantial control over the company. There is no limit to the number of individuals who can be reported for exercising substantial control. An individual exercises substantial control over a reporting company if the individual meets any of four general criteria:

(1) the individual is a senior officer;

(2) the individual has authority to appoint or remove certain officers or a majority of directors of

the reporting company;

(3) the individual is an important decision-maker; or

(4) the individual has any other form of substantial control over the reporting company. See the chart below for

details about these criteria

Chart 3 – Substantial control indicators

SENIOR OFFICER

any individual holding the position or exercising the authority of a:

- President

- Chief financial officer (CFO)

- General counsel (GC)

- Chief executive officer (CEO)

- Chief operating officer (COO)

or any other officer, regardless of official title, who performs a similar function as these officers

APPOINTMENT OR REMOVAL AUTHORITY

any individual with the ability to appoint or remove any SENIOR OFFICER or a majority of the board of directors or similar body

IMPORTANT DECISION-MAKER

any individual who directs, determines, or has substantial influence over important decisions made by the reporting company, including decisions regarding the reporting company's:

1. Business, such as:

- Nature, scope, and attributes of the business

- The selection or termination of business lines or ventures, or geographic focus

- The entry into or termination, or the fulfillment or non-fulfillment, of significant contracts

- Sale, lease, mortgage, or other transfer of any principal assets

- Major expenditures or investments, issuances of any equity, incurrence of any significant debt, or approval of the operating budget

- Compensation schemes and incentive programs for senior officers

- Reorganization, dissolution, or merger

- Amendments of any substantial governance documents of the reporting company, including the articles of incorporation or similar formation documents, bylaws, and significant policies or procedures

CATCH-ALL

any other form of substantial control over the reporting company. Control exercised in new and unique ways can still be substantial. For example, flexible corporate structures may have different indicators of control than the indicators included here

Reporting companies are required to identify all individuals who own or control at least 25 percent of the ownership interests of the company. Any of the following may be an ownership interest: equity, stock, or voting rights; a capital or profit interest; convertible instruments; options or other non-binding privileges to buy or sell any of the foregoing; and any other instrument, contract, or other mechanism used to establish ownership. A reporting company may have multiple types of ownership interests. The following chart identifies the ownership interest types and provides examples.

Chart 4 – Ownership interests

EQUITY, STOCK, OR VOTING RIGHTS

any interest classified as stock or anything similar, regardless whether it confers voting power or voting rights, and even if the interest is transferable EXAMPLES include:

- equity, stock, or similar instrument

- preorganization certificate or subscription transferable share of, or voting trust certificate

- or certificate of deposit for, an equity security, interest in a joint venture, or certificate of interest in a business trust

CAPITAL OR PROFIT INTEREST

any interest in the assets or profits of a company organized as an LLC, which is similar to stock in a corporation and sometimes referred to as a 'unit'

CONVERTIBLE INSTRUMENTS

any instrument convertible into equity, stock, or voting rights or capital or profit interest, whether or not anything needs to be paid to exercise the conversion. The RELATED items are also ownership interests:

- any future on any convertible instrument

- any warrant or right to purchase, sell, or subscribe to a share or interest in equity, stock, or voting rights or capital or profit interest, even if such warrant or right is a debt

OPTION OR PRIVILEGE

any put, call, straddle, or other option or privilege of buying or selling equity, stock, or voting rights, capital or profit interest, or convertible instruments, EXCEPT if the option or privilege is created and held by others without the knowledge or involvement of the reporting company

CATCH-ALL

any other instrument, contract, arrangement, understanding, relationship, or mechanism used to establish ownership

Your company can identify beneficial owners by taking the following steps:

Step 1: Identify individuals who exercise substantial control over the company. Examples are provided below to help you identify those individuals.

Step 2: Identify the types of ownership interests in your company and the individuals that hold those ownership interests. Examples are provided below to help identification.

Step 3: Calculate the percentage of ownership interests held directly or indirectly by individuals to identify individuals who own or control, directly or indirectly, at least 25 percent of the ownership interests of the company.

Here are additional details on each step:

Step 1: Individuals may directly or indirectly exercise substantial control. Individuals can

exercise substantial control through contracts, arrangements, understandings, relationships,

or otherwise.

Note for trusts: a trustee of a

trust or similar arrangement

may exercise substantial

control over a reporting

company

- Board representation.

- Ownership or control of a majority of voting power or voting rights.

- Rights associated with financing or interest.

Examples of indirect ways to exercise substantial control over a reporting company are:

- Controlling one or more intermediary entities that separately or collectively exercise substantial control over a reporting company.

- Through arrangements or financial or business relationships with other individuals or entities acting as nominees.

While keeping these examples in mind, the following questions can help identify which individuals exercise substantial control over your company. Multiple criteria can apply to one individual.

Substantial control question:

Answer

If response is “Yes”:

2. Does your company have any other officers that perform functions similar to those of a President, chief financial officer, general counsel, chief executive officer, or chief operating officer?

Note: One individual may perform one or more functions for a company, or a company may not have an individual who performs any of these functions.

There are senior officers

in your company

3. Does your company have a board of directors or similar body AND does any individual have the ability to appoint or remove a majority of that board or body?

There are individuals with appointment or removal authority over your company.

5. Does any individual direct, determine, or have substantial influence over important decisions made by your company, including decisions regarding your company’s business, finances, or structure?

Note: Certain employees who might fit this description are nevertheless exempt from the beneficial owner definition. See section 2.4 for more information.

There are important decision-makers over your company.

There are individuals to whom the catch-all would apply.

Complete Step 1: Once you have reviewed the examples and questions for exercising substantial control above, you will have enough information to complete Step 1 (identify the individuals who meet the substantial control criteria for your company). The individuals you have identified will be reported as beneficial owners in your company’s BOI report unless they qualify for an exception, as discussed in the next section of the chapter (section 2.4).

Step 2: Individuals may directly or indirectly own or control ownership interests. Individuals can own or control ownership interests through contracts, arrangements, understandings, relationships, or otherwise.

Note for trusts: The following individuals may hold ownership interests in a reporting company through a trust or similar arrangement:

- A trustee or other individual with the authority to dispose of trust assets.

- A beneficiary who is the sole permissible recipient of trust income and principal or who has the right to demand a distribution of or withdraw substantially all of the trust assets.

- A grantor or settlor who has the right to revoke or otherwise withdraw trust assets.

- Joint ownership with one or more other persons of an undivided interest in an ownership interest.

Examples of indirect ways to own or control ownership interests in a reporting company are:

- Owning or controlling one or more intermediary entities, or the ownership interests of any intermediary entities, that separately or collectively own or control ownership interests of a reporting company

- Through another individual acting as a nominee, intermediary, custodian or agent.

While keeping these examples in mind, the following questions can help identify what types of ownership interests are relevant for your company. A company may have more than one type of ownership interest.

Ownership interest question:

Answer

If response is “Yes”:

- an equity security,

- interest in a joint venture, or

- certificate of interest in a business trust?

Your company has ownership interests that are equity, stock, or voting rights.

Your company has ownership interests that are capital or profit interests.

5. Does your company issue any instruments convertible into any share, equity, stock, voting rights, or capital or profit interest?

Note: It does not matter whether anything must be paid to exercise the conversion.

There are important decision-makers over your company.

8. Does your company issue any non-binding put, call, straddle, or other option or privilege of buying or selling equity, stock, or voting rights, capital or

profit interest, or convertible instruments?

Note: Options or privileges created by others without the knowledge or involvement of your company do not apply.

Your company has ownership interests that are options or privileges

8. Does your company have any other instrument, contract, arrangement, understanding, relationship, or mechanism to establish ownership?

The catch-all ownership interest applies to your company.

Complete Step 2: Once you have reviewed the examples and questions for ownership interests above, you will have enough information to complete Step 2 (identify the individuals who hold ownership interests in your company). Step 3 will help you identify which of these individuals own or control 25 percent or greater of the ownership interests in your company. The individuals who own or control 25 percent or more of the ownership interests in your company will be reported as beneficial owners in your company’s BOI report unless they qualify for an exception, as discussed in the next section of the chapter (section 2.4).

Step 3: After identifying what types of ownership interests apply to your company and who owns or controls them, you must determine who owns or controls 25 percent or more of those ownership interests.

If your company has issued any options, privileges, or convertible instruments:

- Assume they have been exercised or converted in all calculations below.

- Calculate each individual’s ownership interest as a percentage of the total shares of stock issued. If some shares of stock that your company issues have more voting power or represent more of the value of the company than other shares (for instance, if your company issues both series A shares with one vote per share and series B shares with ten votes per share), you will need to make the following two calculations. The individual’s ownership interest will be the larger of the two percentages:

÷

Total outstanding voting power of all classes of ownership interests entitled to vote=

Individual’s voting power %Total combined value of the individual’s ownership interests

÷

Total outstanding value of all classes of ownership interests

=

Individual’s ownership interest value %

If your company, including if your company is treated as a partnership for federal income tax purposes, issues capital or profit interests:

- Apply the following calculation:

÷

Total outstanding capital and profit interests

=

Individual’s capital and profit interests %

- Identify any individual who owns or controls 25 percent or more of any class or type of ownership interest of the company.

Complete Step 3: After you have applied these scenarios to your company’s ownership interests, you will have enough information to identify the individuals who own or control 25 percent or greater of the ownership interests in your company. You must report the individuals who own or control 25 percent or more of the ownership interests in your company as beneficial owners in your company’s BOI report unless they qualify for an exception, as discussed in the next section of the chapter (section 2.4).

Examples of how to determine beneficial owners:

The following examples show how to determine beneficial owners across a variety of types of company structures. These examples assume that no exceptions apply to the beneficial owners, as discussed in the next section of the chapter (section 2.4). In the infographics for the examples, beneficial owners are noted by circles and non-beneficial owners are noted by triangles.

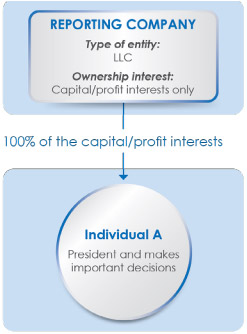

Example 1: The reporting company is a limited liability company (LLC). Individual A is the sole owner and president of the company and makes important decisions for the company. No one else owns or controls ownership interests in the company or exercises substantial control over the company

Individual A is a beneficial owner of the reporting company in two different ways, assuming no other facts. First, Individual A exercises substantial control over the company because Individual A is a senior officer of the company (the president). Second, Individual A is also a beneficial owner because Individual A owns 25 percent or more of the reporting company’s ownership interests.

Because no one else owns or controls ownership interests in the LLC or exercises substantial control over it, and assuming there are no other relevant facts, Individual A is the only beneficial owner of this reporting company, and Individual A’s information must be reported to FinCEN.

Example 2: The reporting company is a corporation. The company’s total outstanding ownership interests are shares of stock. Three people (Individuals A, B, and C) own 50 percent, 40 percent, and 10 percent of the stock, respectively, and one other person (Individual D) acts as the president, for the company, but does not own any stock.

Assuming there are no other relevant facts, Individuals A, B, and D are all beneficial owners of the

company and their information must be reported. Individual C is not a beneficial owner.

Individual A owns 50 percent of the company’s stock and therefore is a beneficial owner because 50 percent is greater than the threshold of 25 percent or more of the company’s ownership interests

Individual B owns 40 percent of the company’s stock and therefore is a beneficial owner 40 percent is also greater than the threshold of 25 percent or more of the company’s ownership interests.

Individual C is not a senior officer of the company and does not directly or indirectly exercise any substantial control over the company

Individual C also owns 10 percent of the company’s stock, which is less than the 25 percent or greater interest needed to qualify as a beneficial owner by virtue of ownership interests. Individual C is therefore not a beneficial owner of the company

Individual D is president of the company. As a senior officer of the company, Individual D exercises substantial control over the company and is therefore a beneficial owner, regardless of whether or not Individual D owns or controls 25 percent or more of the company’s ownership interests.

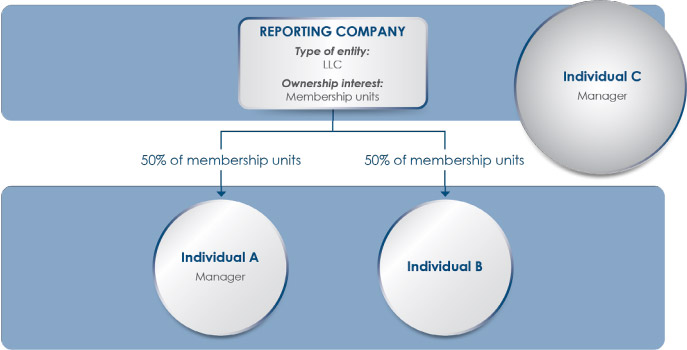

Example 3: The reporting company is an LLC with two managers, Individuals A and C. Individual A also owns 50 percent of the “membership units” in the LLC while Individual C does not. Individual B owns the remaining membership units in the LLC but is not a manager

Owners of membership units (which are a type of “capital or profit interest” ownership interest) in an LLC are sometimes called “members” of the LLC. A member may not automatically be required, or authorized, to make decisions for the LLC; depending on the internal organization of the LLC, however, a member may also be a “manager.” In this example, Individual A is a member and a manager. Individual B is a member but not a manager, while Individual C is a manager but not a member. All three are beneficial owners of the reporting company

Individual A is a manager of the LLC and owns 50 percent of the company’s membership units. Individual A exercises substantial control over the LLC because Individual A makes important decisions for the LLC in the role of manager. Individual A also owns 50 percent (which is greater than the 25 percent or more threshold) of the company’s ownership interests. Individual A is therefore a beneficial owner of the reporting company in two different ways, by exercising substantial control and owning or controlling 25 percent or more of the ownership interests.

Individual B owns 50 percent (which is greater than the 25 percent or more threshold) of the LLC’s membership units. That makes Individual B a beneficial owner of the LLC even though Individual B is not a manager and does not make important decisions or otherwise exercise substantial control over the LLC.

Individual C is a manager of the LLC and makes important decisions on its behalf, thereby exercising substantial control over it. Individual C does not own any of the LLC’s membership units (the ownership interests) but is nevertheless still a beneficial owner because the individual exercises substantial control.

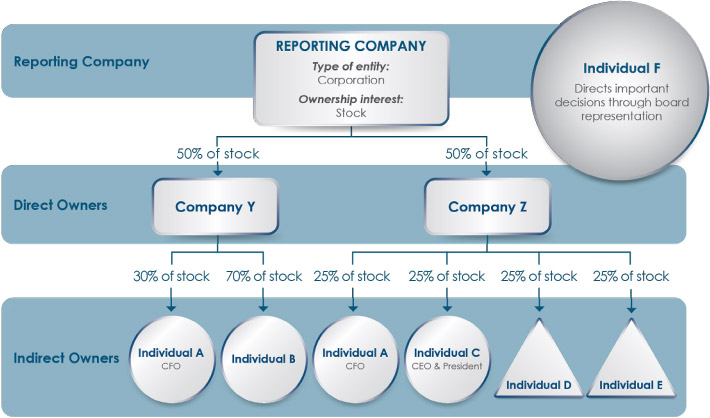

Example 4: A reporting company is a corporation with multiple indirect owners through Company Y and Company Z

In this example, Individuals A, B, C, and F are beneficial owners.

Individual A is the reporting company’s Chief Financial Officer and is therefore a senior officer, which under the Reporting Rule means that Individual A exercises substantial control over the company. Individual A also indirectly owns 27.5 percent of the reporting company’s stock through direct ownership of Company Y and Company Z, which each own 50 percent of the reporting company’s stock. (Individual A owns 30 percent of Company Y’s stock and 25 percent of Company Z’s stock. Therefore, Individual A owns 15 percent of the reporting company’s stock through Company Y (50% × 30% = 15%) and 12.5 percent of the reporting company’s

stock through Company Z (50% × 25% = 12.5%). Adding these two percentages together equals 27.5 percent of the reporting company’s stock.) Individual A is therefore a beneficial owner in two different ways, by exercising substantial control and owning or controlling 25 or more of the ownership interests of the reporting company.

Individual B indirectly owns 35 percent of the reporting company’s stock through Company Y, which owns 50 percent of the reporting company’s stock. (Individual B owns 70 percent of Company Y’s stock (50% × 70% = 35%)). Individual B does not exercise substantial control. Individual B is a beneficial owner by owning or controlling 25 percent or more of the reporting company’s ownership interests.

Individual C is the reporting company’s Chief Executive Officer and president and is therefore a senior officer who exercises substantial control. Individual C indirectly owns 12.5 percent of the reporting company’s stock. To calculate Individual C’s indirect ownership interests in the reporting company, multiply the ownership interest of Individual C in Company Z by the ownership interest of Company Z in the reporting company. Individual C owns 25 percent of Company Z’s stock and Company Z owns 50 percent of the reporting company’s stock. Therefore, Individual’s C ownership interests in the reporting company are 12.5 percent (25% × 50% = 12.5%), which is less than the 25 percent ownership interest threshold. Accordingly, Individual C’s ownership interests in the reporting company do not make Individual C a beneficial owner, but Individual C is nevertheless a beneficial owner because Individual C exercises substantial control over the reporting company.

Similar to Individual C, Individuals D and E own 25 percent of Company Z’s stock, and each therefore indirectly owns 12.5 percent of the reporting company’s stock. In contrast to Individual C, Individuals D and E do not exercise substantial control over the reporting company. Individuals D and E are not beneficial owners.

Individual F is on the company’s board of directors and makes important decisions on the reporting company’s behalf, thereby exercising substantial control over it. Individual F does not own or control any stock in the reporting company. Individual F is therefore a beneficial owner by exercising substantial control over the reporting company, but not through holding ownership interests in it.

There are five exceptions to the definition of beneficial owner. When an individual who would otherwise be a beneficial owner of a reporting company qualifies for an exception, the reporting company does not have to report that individual as a beneficial owner in its BOI report to FinCEN. The following checkboxes are intended to help your company determine whether any exceptions apply to individuals who might otherwise qualify as beneficial owners of your company.

Minor Child (Exception #1)

1. The individual is a minor child, as defined under the law of the State or Indian tribe in which the domestic reporting company is created or the foreign reporting company is first registered.

Special rule for minor child: If the answer above is yes, the reporting company may instead report information about the parent or legal guardian of the minor child.

Note: This exception only applies if a parent or legal guardian’s information is reported in lieu of the minor child’s information. Also, when the minor child reaches the age of majority, as defined by the law of the State or Indian tribe in which the reporting company was created or first registered, the exception no longer applies. At that time, if the individual is a beneficial owner, the reporting company must file an updated BOI report providing the individual’s own information. See Chapter 6 for more information on when an updated report may be required.

Nominee, intermediary, custodian, or agent (Exception #2)

2. The individual merely acts on behalf of an actual beneficial owner as the beneficial owner’s nominee, intermediary, custodian, OR agent.

Note: Individuals who perform ordinary advisory or other contractual services (such as tax professionals) likely qualify for this exception. In scenarios where this exception applies, the actual beneficial owner must still be reported.An individual qualifies for this exception if all three of the following criteria apply:

1. The individual is an employee of the reporting company, when applying the meaning of “employee” provided in 26 CFR 54.4980H-1(a)(15). In general, the term employee means that an individual is subject to the will and control of the employer in what and how to do work, and that the employer may discharge the individual from work.

3. The individual is not a senior officer of the reporting company. The term “senior officer” means any individual holding the position or exercising the authority of a president, chief financial officer, general counsel, chief executive officer, or chief operating officer, or any other officer, regardless of official title, who performs a similar function.

Inheritor (Exception #4)

An individual qualifies for this exception if the following criterion applies:

1. The individual’s only interest in the reporting company is a future interest through a right of inheritance, such as through a will providing a future interest in a company

Note: Once the individual inherits the interest, this exception no longer applies, and the individual may qualify as a beneficial owner. See Chapter 6 for more information on when an updated report may be required in this circumstance.

An individual qualifies for this exception if the following criterion applies:

1. The individual is a creditor of the reporting company. The term “creditor” means an individual who would meet the definition of a beneficial owner of the reporting company solely through rights or interests for the payment of a predetermined sum of money, such as a debt incurred by the reporting company, or a loan covenant or other similar right associated with such right to receive payment that is intended to secure the right to receive payment or enhance the likelihood of repayment.

For example, an individual qualifies for the creditor exception if the individual is entitled to payment from the reporting company to satisfy a loan or debt, so long as this entitlement is the only ownership interest the individual has in the reporting company